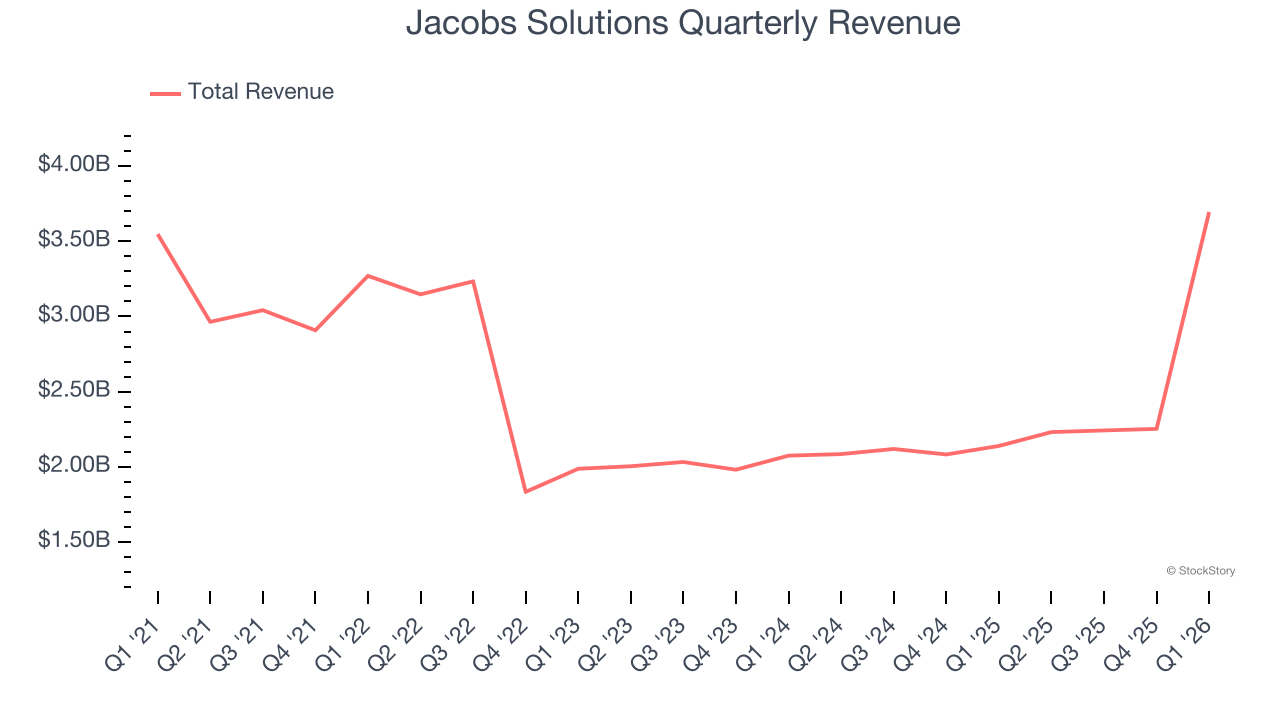

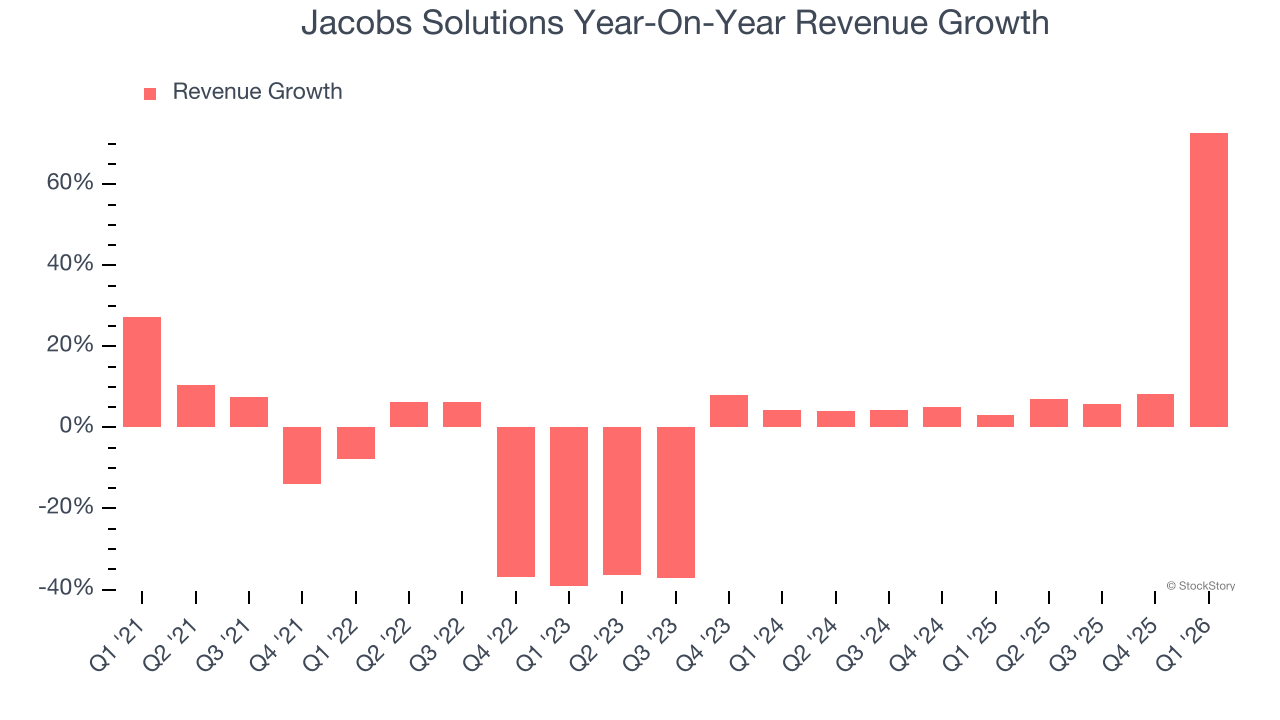

Global professional services company Jacobs Solutions (NYSE:J) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 72.7% year on year to $3.69 billion. Its non-GAAP profit of $1.75 per share was 7.1% above analysts’ consensus estimates.

Is now the time to buy Jacobs Solutions? Find out by accessing our full research report, it’s free.

Jacobs Solutions (J) Q1 CY2026 Highlights:

- Revenue: $3.69 billion vs analyst estimates of $2.28 billion (72.7% year-on-year growth, 61.9% beat)

- Adjusted EPS: $1.75 vs analyst estimates of $1.63 (7.1% beat)

- Adjusted EBITDA: $327.2 million vs analyst estimates of $319.8 million (8.9% margin, 2.3% beat)

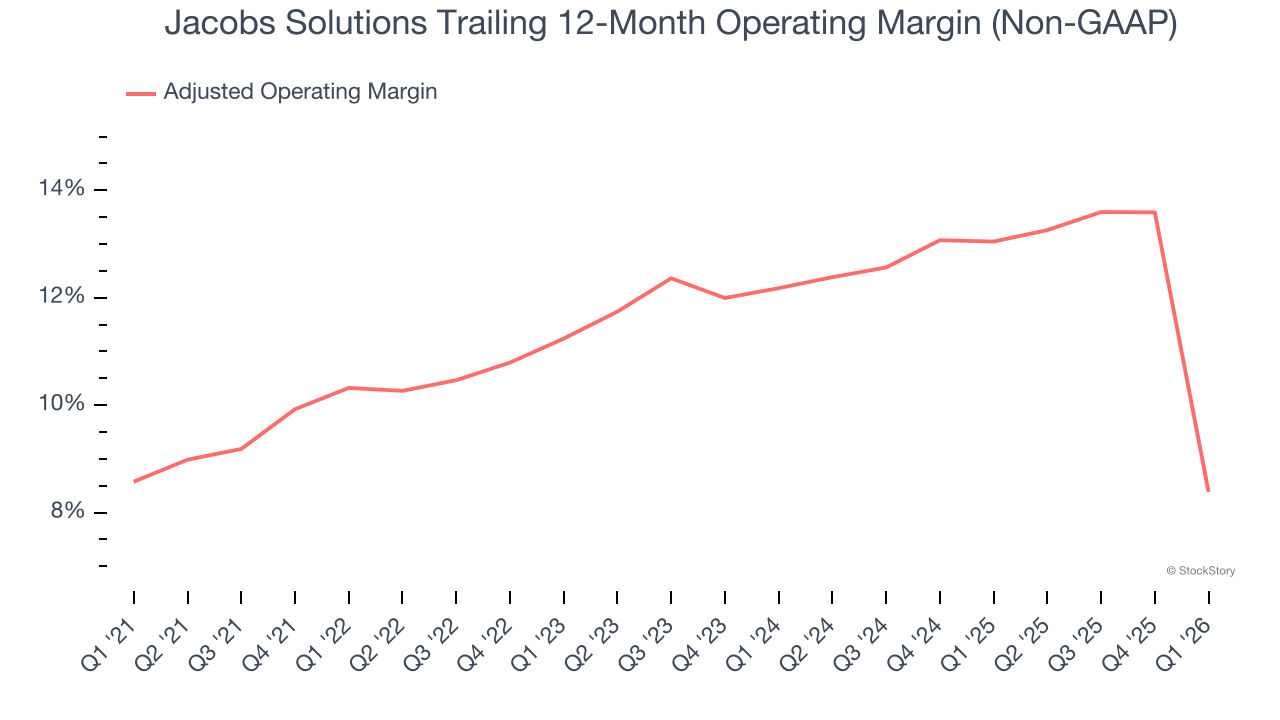

- Operating Margin: -2.2%, down from 9.8% in the same quarter last year

- Free Cash Flow was -$504.9 million compared to -$113.7 million in the same quarter last year

- Backlog: $26.97 billion at quarter end

- Market Capitalization: $15.35 billion

Company Overview

With a workforce of approximately 45,000 professionals tackling complex challenges from water scarcity to cybersecurity, Jacobs Solutions (NYSE:J) provides engineering, consulting, and technical services focused on infrastructure, sustainability, and advanced technology solutions.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $10.42 billion in revenue over the past 12 months, Jacobs Solutions is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For Jacobs Solutions to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Jacobs Solutions’s demand was weak over the last five years. Its sales fell by 3.5% annually, a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Jacobs Solutions’s annualized revenue growth of 13.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Jacobs Solutions reported magnificent year-on-year revenue growth of 72.7%, and its $3.69 billion of revenue beat Wall Street’s estimates by 61.9%.

Looking ahead, sell-side analysts expect revenue to decline by 6.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Jacobs Solutions has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 10.9%, higher than the broader business services sector.

Analyzing the trend in its profitability, Jacobs Solutions’s adjusted operating margin decreased by 1.9 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Jacobs Solutions become more profitable in the future.

This quarter, Jacobs Solutions generated an adjusted operating margin profit margin of negative 1.6%, down 14.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

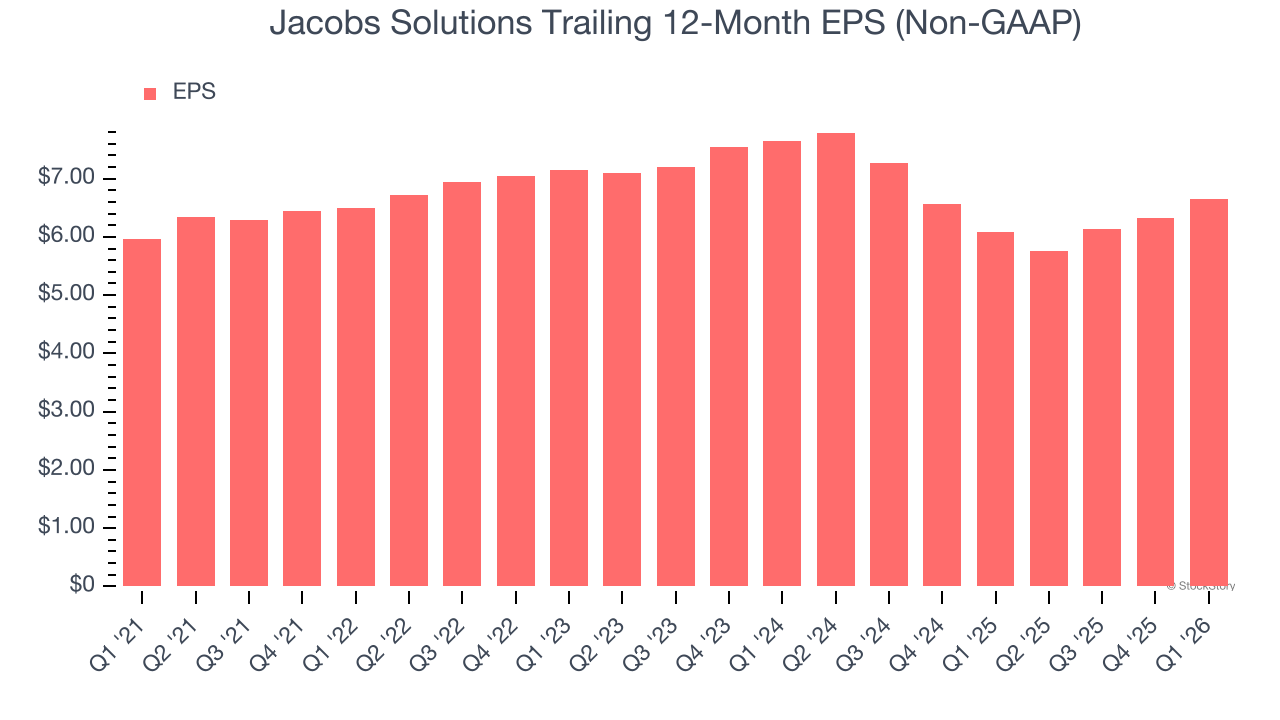

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Jacobs Solutions’s EPS grew at 2.2% compounded annual growth rate over the last five years. This performance was better than its 3.5% annualized revenue declines but doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

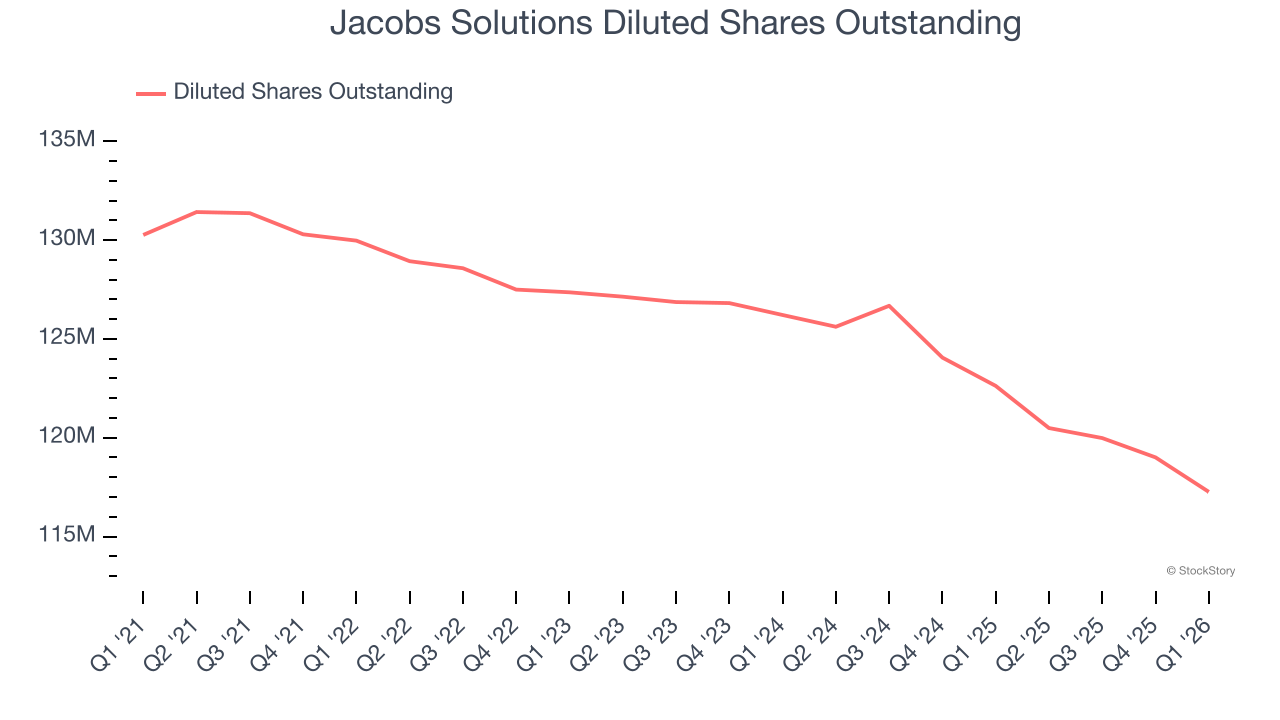

We can take a deeper look into Jacobs Solutions’s earnings to better understand the drivers of its performance. A five-year view shows that Jacobs Solutions has repurchased its stock, shrinking its share count by 10%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Jacobs Solutions, its two-year annual EPS declines of 6.8% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Jacobs Solutions reported adjusted EPS of $1.75, up from $1.43 in the same quarter last year. This print beat analysts’ estimates by 7.1%. Over the next 12 months, Wall Street expects Jacobs Solutions’s full-year EPS of $6.65 to grow 13.7%.

Key Takeaways from Jacobs Solutions’s Q1 Results

EBITDA and EPS beat analysts’ expectations this quarter, although it's unclear if all estimates reflect correct acquisition timing. The stock remained flat at $135.47 immediately after reporting.

So do we think Jacobs Solutions is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).